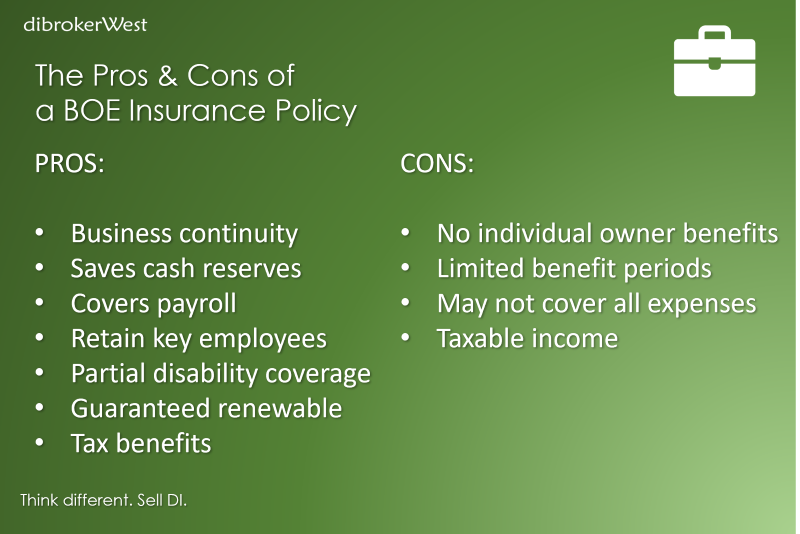

Choosing the right Business Overhead Expense (BOE) disability insurance policy can keep your clients’ business open if the owner becomes disabled. BOE is a specialized disability insurance product that covers essential monthly expenses such as rent, employee salaries, utilities and more—ensuring the business can stay afloat during the owner’s recovery.

When helping your client select a BOE policy, it’s critical to evaluate the business’s overhead structure and potential risks. Here are the key factors to consider.

Start by calculating the business’s fixed monthly expenses—the costs that persist even if the owner can’t work. These expenses will determine the amount of coverage needed. Common overhead expenses include:

A clear understanding of average monthly overhead ensures you recommend the right coverage amount to meet real financial needs.

The waiting period (also elimination period) is the time the insured must be disabled before benefits begin. Most BOE policies offer options ranging from 30 to 90 days.

Consider your client’s cash reserves and the business’s ability to weather a temporary revenue gap.

BOE policies typically provide benefits for 12 to 24 months. Choosing the right benefit period depends on:

Smaller, less complex businesses may only need 12 months of coverage, while larger or more dependent operations might benefit from a full 24-month term.

Every policy contains exclusions and limitations. Common exclusions include:

It’s also important to review benefit caps for specific categories—such as rent or wages. Carefully review these with your client to avoid surprises during claim time.

Riders can enhance BOE policies to meet specific business needs. Consider:

If your client is actively growing their business or has unpredictable income, riders like the future increase option may be especially valuable.

Premiums vary based on factors like:

Many carriers offer business overhead expense premium discounts if the product is bundled with personal disability or other business insurance. Check with your dibrokerWest Sales Rep to explore any available business-owner or multi-policy discounts.

Policy terms are only as reliable as the company behind them. Ensure your client’s BOE policy comes from an insurer with:

Working with a carrier known for financial stability and excellent customer support adds peace of mind for you and your client.

Business overhead expense disability insurance is a smart way to protect your client’s livelihood—and the livelihoods of their employees. Taking the time to select the right policy ensures the business can continue to operate during the owner’s recovery. Reach out to your dibrokerWest team for help designing the right plan for your client’s unique business structure.